Asset Allocation

(7 of 8)

Asset Allocation

Asset allocation involves identifying how much of your investment portfolio will be distributed amongst various asset classes or types of investments like stocks, bonds, and cash. When determining what percentage of your investment dollars to allocate to stocks, bonds, and cash, consider the factors listed below.

Things To Know

- The longer your time horizon, the more aggressive you can be with your investment dollars.

- Determining risk tolerance is a very personal decision for each investor.

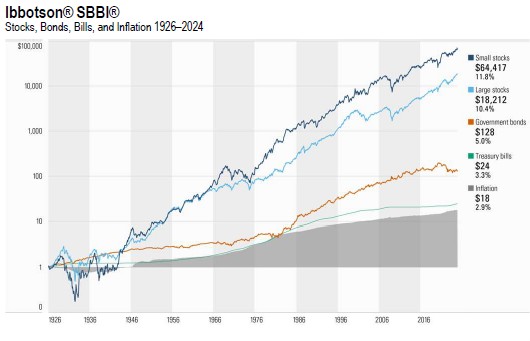

Time horizon

Generally speaking, the longer the investor’s time horizon (length of time to invest), the more aggressive they can be with allocating investment dollars to growth investments like stocks. While stock prices can experience large swings up and down over a short period of time like one year, they have generally performed well and demonstrated a very low probability of loss when held over longer periods of time. The chart below illustrates this concept.

For illustrative purposes only. The illustrative returns shown above do not reflect the investment or performance of an actual portfolio. Source: Financial Fitness Group.

Risk tolerance

Determining risk tolerance is a very personal decision for each investor. Some investors are simply more conservative than others. A good way to consider how much risk you are willing to take is to determine how much volatility you are willing to accept in your portfolio. This can be evaluated by determining how much you would be willing to see the value of your portfolio decline without needing to sell and take a loss.

Review the chart below to help bring this concept to life. Keep in mind that you only incur the loss if you actually sell the investment.

What would you do if this were your portfolio, assuming you didn’t need access to this money in the next 5 years?

For illustrative purposes only. The illustrative account statement shown above does not reflect the investment or performance of an actual portfolio. Source: Financial Fitness Group.

Investment goals

The type of an investment goal an investor has often should dictate what type of risk they take on in their investment portfolio. For example, if an investor needs money for their child’s college education in 10 years, they may choose a more conservative or moderate approach to investing. While 10 years is considered a long-term investment time frame, the investor will need to withdraw funds at a specific time in the future to pay for college expenses. They don’t have the luxury of riding out a downturn if their child’s tuition bill is due.

Conversely, someone who is investing for retirement 30 years from now can afford to be more aggressive with their investment portfolio. Even if their portfolio is experiencing a downturn in the first year of their retirement, they don’t have a need to withdraw all of their retirement savings at once. So the bulk of their dollars will have an opportunity to weather the downturn.

Asset allocation and diversification often are thought of as the same thing. However, they are different concepts. As we just learned, asset allocation is associated with determining how much you will allocate to an asset class like stocks, bonds, and cash. Diversification is associated with the allocation of investment dollars within each of those asset classes. For example, within the stock allocation, investments could be diversified into stocks based on the size of the company: 50% large, 30% mid, and 20% small-sized companies. This further reduces risk within each asset class.

Asset allocation portfolio examples

As we have discussed, before making any investment decisions be sure you are comfortable with your strategy and the risks involved with your portfolio. Again, many investors work with a financial advisor to develop and implement an investment plan.

We’ll leave you with a few generic asset allocation portfolio examples based on different risk tolerance levels. This is only a guide, and your personal investment plan should be based on your financial goals and individual risk tolerance level.

For illustrative purposes only. This material should not be viewed as advice or recommendations with respect to asset allocation or any particular investment. This information is not intended to, and should not, form a primary basis for any investment decisions that you may make. Source: Financial Fitness Group.