Potential Shortfall: The Risk of High Withdrawal Rates

Potential Shortfall: The Risk of High Withdrawal Rates

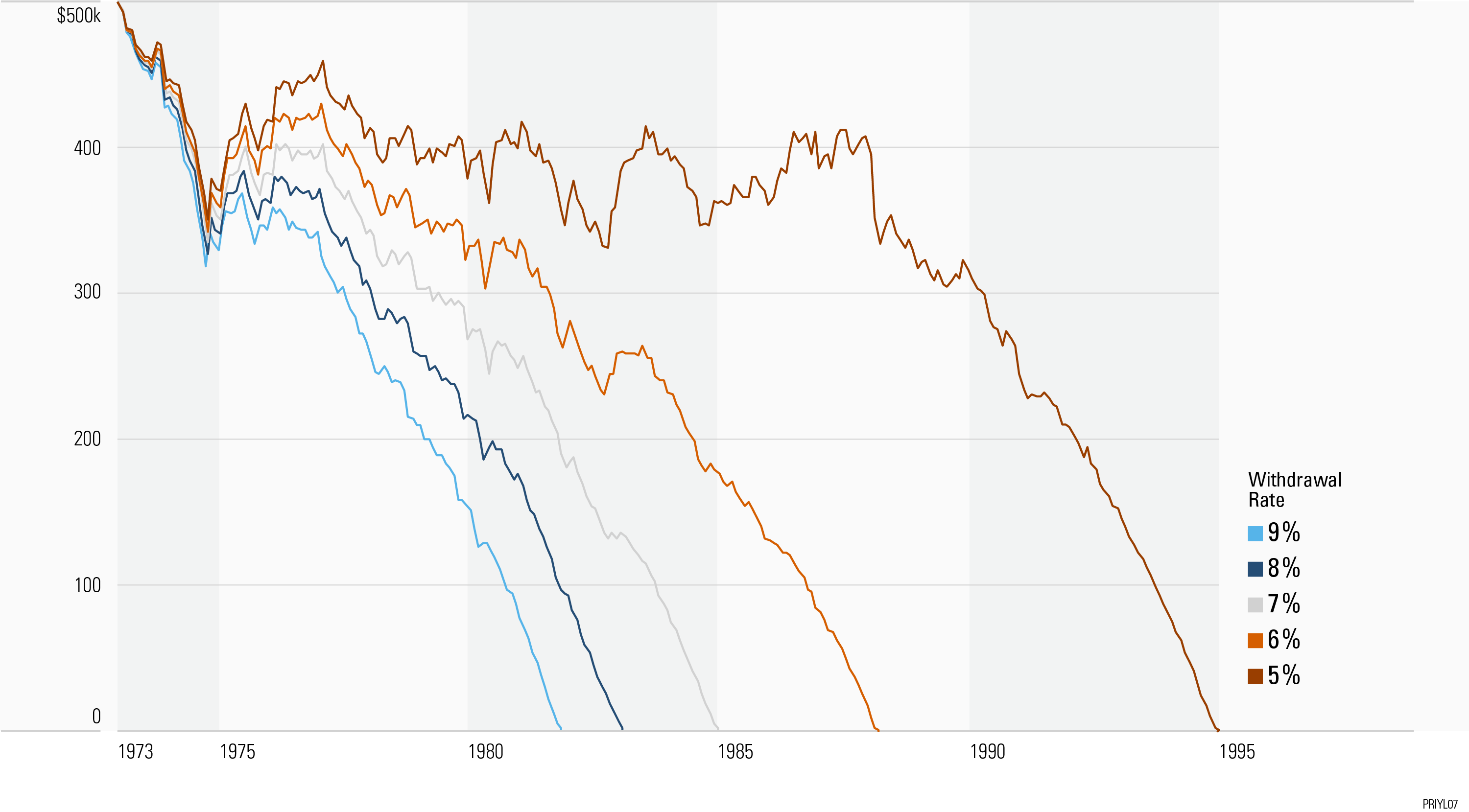

If you plan on withdrawing from your retirement savings for a long period of time, it is important to examine the effect various withdrawal rates may have on a portfolio.

Several factors need to be examined when determining an investor’s withdrawal rate. The answer may depend upon the portfolio mix, how long an investor expects to withdraw from the portfolio, and the investor’s risk aversion and consumption patterns.

This image looks at a hypothetical 50% stock/50% bond portfolio and the effect various inflation-adjusted withdrawal rates have on the end value of the portfolio over a long payout period. The hypothetical portfolio has an initial starting value of $500,000. It is assumed that a person retires on Dec. 31, 1972, and withdraws an inflation-adjusted percentage of the initial portfolio wealth ($500,000) each year beginning in 1973.

As illustrated, the higher the withdrawal rate, the greater the chance of potential shortfall. The lower the rate, the less likely you are to outlive your portfolio. Therefore, early retirees who anticipate long payout periods may want to consider assuming lower withdrawal rates.

Things To Know

- Early retirees who anticipate long payout periods may want to consider assuming lower withdrawal rates.

Market forces also have an effect on withdrawal rates. The 1973 start date was chosen to illustrate how investing right before a significant market downturn could impact the subsequent evolution of the portfolio with various withdrawal rates.

Diversification does not eliminate the risk of investment losses. Government bonds are guaranteed by the full faith and credit of the U.S. government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes.

About the data

Stocks in this example are represented by the Ibbotson® Large Company Stock Index. Bonds are represented by the five-year U.S. government bond and inflation by the Consumer Price Index. An investment cannot be made directly in an index. Each monthly withdrawal is adjusted for inflation. Each portfolio is rebalanced monthly. Assumes reinvestment of income and no transaction costs or taxes.