Potential to Reduce Risk or Increase Return

Potential to Reduce Risk or Increase Return

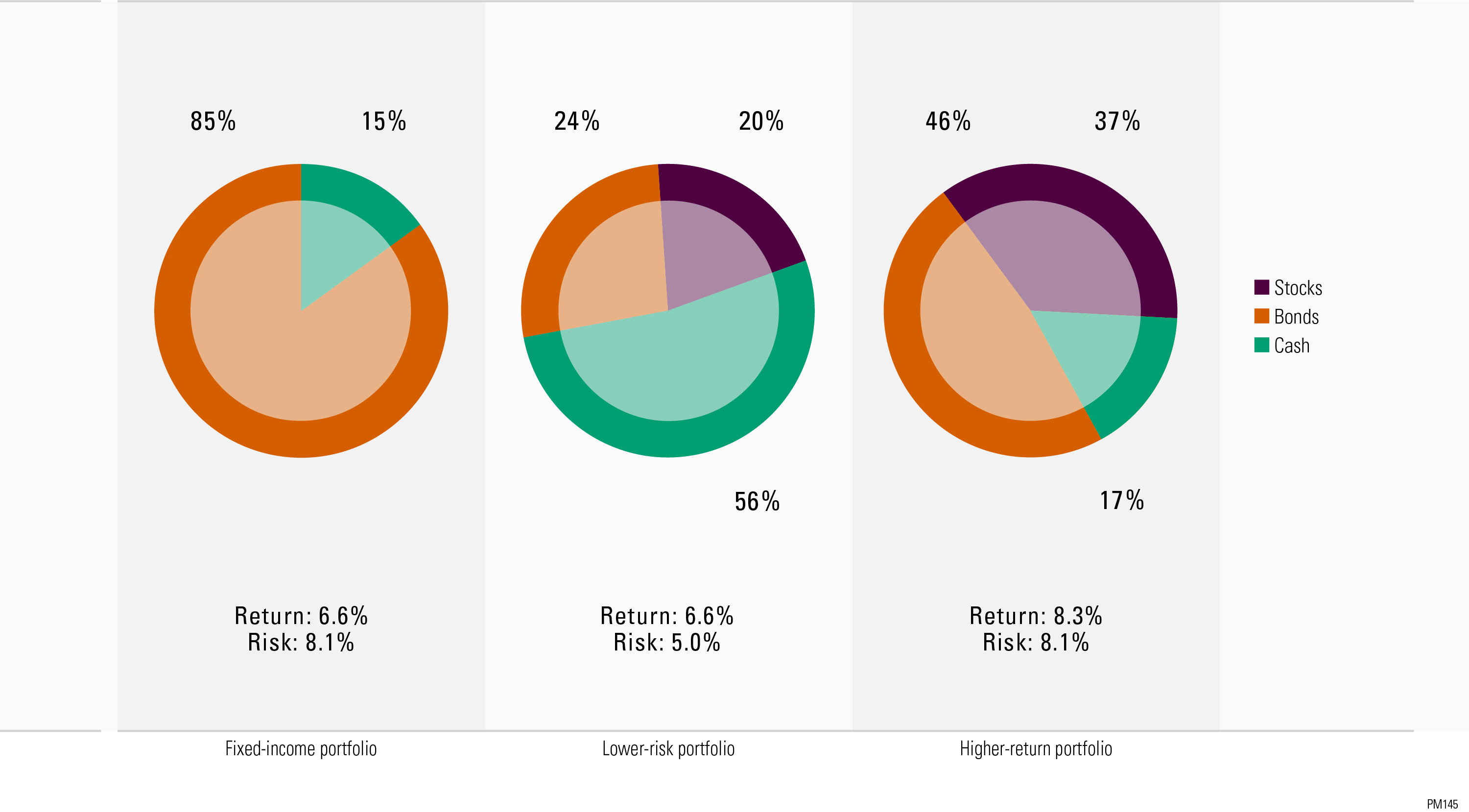

Historically, adding stocks to a portfolio of less volatile assets reduced risk without sacrificing return or increased return without assuming additional risk.

This image illustrates the risk-and-return profiles of three hypothetical investment portfolios. The lower-risk portfolio, which included stocks, had the same return as the portfolio composed entirely of fixed-income investments but assumed less risk. The higher-return portfolio had the same risk level as the fixed-income portfolio, but produced an increased return.

The value of adding stocks

Although it may appear counterintuitive, diversifying a portfolio of fixed-income investments to include stocks reduced the overall volatility of a portfolio during the time period analyzed. Likewise, it is possible to increase your overall portfolio return without having to take on additional risk.

Because stocks, bonds, and cash generally do not react identically to the same economic or market stimuli, combining these assets can often produce a more appealing risk/return tradeoff.

Things To Know

- It is possible to increase your overall portfolio return without having to take on additional risk.

Diversification does not eliminate the risk of experiencing investment losses. Government bonds and Treasury bills are guaranteed by the full faith and credit of the US government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes.

About the data

Stocks are represented by the Ibbotson® Large Company Stock Index. Long-term government bonds are represented by the 20-year U.S. government bond, intermediate-term government bonds by the five-year U.S. government bond, and cash by the 30-day U.S. Treasury bill. Bonds represent an equally weighted portfolio of long-term government bonds and intermediate-term government bonds. All portfolios are rebalanced annually. Risk is measured by standard deviation. Standard deviation measures the fluctuation of returns around the arithmetic average return of the investment. The higher the standard deviation, the greater the variability (and thus risk) of the investment returns. An investment cannot be made directly in an index. The data assumes reinvestment of all income and does not account for taxes or transaction costs.