Reasons to Invest

(2 of 8)

Reasons to Invest

If you had to come up with a single reason why investing is important, it would be so you can achieve your future financial goals. With the exception of those young adults who begin their independent life with substantial assets, most of us will be required to save a portion of our income as well as invest it wisely to help us meet our future financial needs.

Let’s take a little closer look at a few important reasons to invest.

Reason 1: Grow your money through compounding

Who doesn’t like to see their money grow over time? Most people do, so they have an opportunity to use this money in the future to cover a need or want.

Compound interest is interest added to the principal (the amount you deposited or invested) of a deposit so that the added interest also earns interest from then on. This addition of interest to the principal is called compounding. The most common accounts that pay interest are savings, money markets, and certificates of deposit. It can also be referred to as compound growth. The same compounding principal applies for compound growth but the types of products used are stocks and mutual funds. More on those products shortly.

A more informal definition for compound interest is, "The money you invest makes money, and the money you make on the money you invest makes money, and so on."

The earlier you start investing, the more powerful the investing typically is. Take a look at the chart below to see how compounding works.

How much you need to save monthly based on what age you begin saving to get to $1 million

Growth rates will vary and may be negative. Actual results may differ substantially from that shown. This illustration is hypothetical and is not meant to represent any specific investment or imply any guaranteed rate of return. Source: Financial Fitness Group. Disclosure.

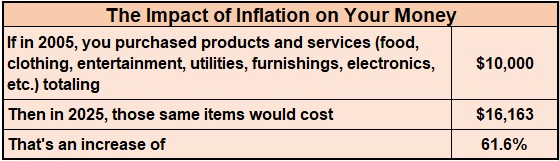

Reason 2: Inflation

Inflation can be defined as the rate at which the general level of prices for goods and services is rising, which in turn means the purchasing power of currency is falling. It simply means that the things we buy will generally increase in price in the future. Our cost of living will rise; therefore our money today won’t be worth as much in the future.

Inflation is stated as a percentage. Over the last 100 years the inflation rate averaged approximately 3% (source: Inflationdata.com). So on average, the cost of living, or how much we pay for goods and services in a year, increased by 3%. In number terms, it means for every $10,000 we spend on goods and services this year, we will need to spend $10,300 (a 3% increase) in order to purchase the same goods and services next year.

Let’s take a look at a how prices have inflated over the last 20 years:

For illustrative purposes only. The illustrative figures shown above do not reflect real cost-of-living figures. Source: Financial Fitness Group. Data from Bureau of Labor Statistics consumer price index.

Reason 3: Achieve your goals

Investing wisely will help you increase the likelihood of achieving your financial goals. Most of us look forward to having enough money to cover the needs we have over our lifetime. Many of our future needs have a price tag associated with them, and it is a combination of saving and investing that helps make these goals a reality. Review the list of goal categories detailed below and ask yourself which of these may be important to you:

- Major purchases like home, car, furnishings, remodeling project, boat, snowmobile, four-wheeler.

- Start a business: This takes money/capital to lease or buy a building, purchase equipment, advertise, hire employees, etc.

- Family: Are children in your future? While having children can be one of the greatest joys in life, children increase your expenses for the basics like food, clothing, and utilities. If you want to help pay for college for your children, you will need to save and invest additional dollars.

Additionally, if you need or want to help cover expenses for family members in need, be sure to invest to cover these future needs.

When setting financial goals related to reaching a specific dollar amount to accumulate, consider the following factors:

.

Interest/growth rates will vary and may be negative. Actual results may differ substantially from that shown. This illustration is hypothetical and is not meant to represent any specific investment or imply any guaranteed rate of return. Source: Financial Fitness Group.

Reason 4: Financial independence

Often called retirement, this is likely the most expensive goal you will need to provide for during your life. When you retire, you are responsible for paying yourself an income for the rest of your life, which is hopefully 20–30 years depending on when you choose to retire. For most, the two primary sources of income during retirement are:

- Social Security: the amount of income you receive from Social Security directly corresponds to the amount of Social Security tax withheld from your income during your earning years. Social Security payments were never intended to provide the majority of someone’s retirement income. Those who live only on Social Security generally have a tight budget.

- Investments: the majority of a retiree’s income comes from money specifically saved and invested for retirement. This is money that you and/or your employer have contributed to an investment plan with a goal of accumulating money that can be tapped to produce income for you during retirement. These investment plans generally are in the form of a qualified retirement plan where participants receive tax benefits while they are contributing to the plan and employers contribute to the plan. Oftentimes, individuals will have other investment accounts in addition to their retirement plans.

Understanding how much you can withdraw each month during retirement from your investment account(s) is critical to ensuring you don’t outlive your assets. If you withdraw too much money each month, you risk running out of money.

Investment/growth rates will vary and may be negative. Actual results may differ substantially from that shown. This illustration is hypothetical and is not meant to represent any specific investment or imply any guaranteed rate of return. Source: Financial Fitness Group.

Investing is all about preparing to accumulate funds for a planned future expense. For most, the investment objective during the working years is growth. During retirement the investment objective changes to generating income from the investments you have accumulated during your working years.

Before you rush to your broker and start buying, you have some thinking and planning to do. To choose from the growing universe of investment choices, you have to understand which types of investments are the best match for your goals and your investment personality. The potential risks and rewards can differ greatly based on the investment option.